Founder Education Series

How SAFE Financing Works

Every dollar you raise changes what you own, who controls your company, and who gets paid first at exit. This guide walks you through the full picture — from your first SAFE to Series B — so you understand every tradeoff before you sign.

Visual Reference

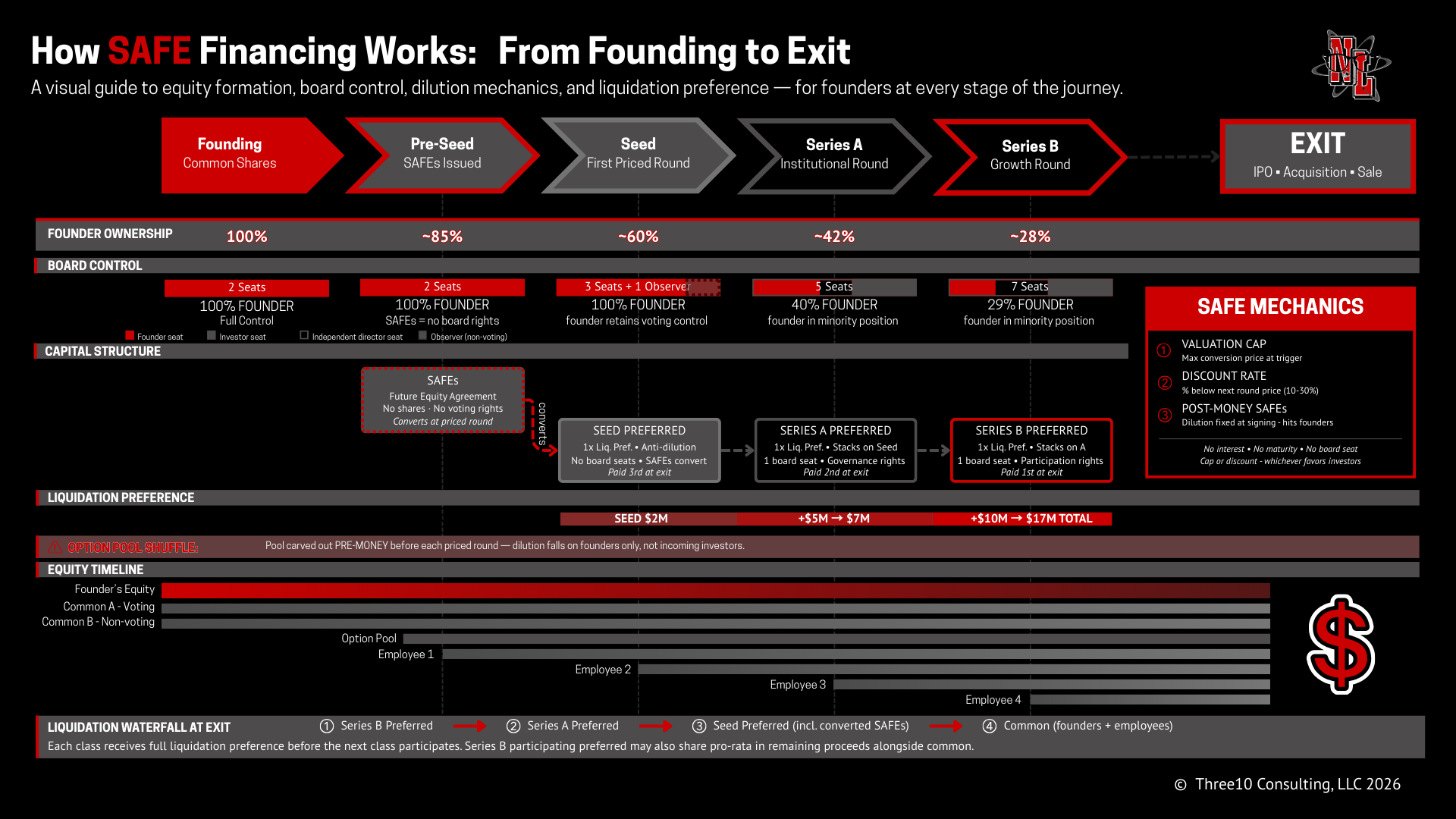

The full Picture

Everything on one chart — equity structure, board control, liquidation preference, and how SAFEs convert. Reference this at every stage of your fundraise.

the instrument

What is a SAFE?

A SAFE — Simple Agreement for Future Equity — is a contract that lets an investor put money into your startup today in exchange for the right to receive shares later, when you raise a priced round. It was created by Y Combinator in 2013 as a faster, cheaper alternative to convertible notes.

When you issue a SAFE, the investor doesn't get shares immediately. They get a promise: when your company raises its first priced round (typically Seed or Series A), their investment converts into preferred shares at a discount or capped price. Until then, they hold no equity, have no voting rights, and sit on no board.

The key insight: SAFEs feel simple on the way in. But every SAFE you issue is a future dilution event waiting to happen — and the timing, size, and terms of that dilution are often poorly understood by founders until it's too late to negotiate.

Valuation Cap

The maximum company valuation at which your SAFE will convert. If your cap is $5M and you raise a Seed at a $10M valuation, SAFE holders convert as if the company were worth $5M — getting twice as many shares as new investors at the same price.

Discount Rate

A percentage reduction off the next round's price per share — typically 10–30%. A 20% discount means the SAFE holder pays $0.80 for every $1.00 share the new investors pay. The investor uses whichever term — cap or discount — gives them more shares.

Post-Money SAFEs

The current YC standard. The SAFE holder's ownership percentage is calculated after the SAFE is issued — meaning dilution is fixed at the time you take the money, not at conversion. This is predictable for investors and often overlooked by founders who don't model it out.

Conversion Trigger

SAFEs convert automatically at the first "equity financing" above a minimum threshold — usually $1M. Until that trigger fires, SAFE holders hold no shares, attend no board meetings, and receive no financial statements unless you voluntarily share them.

the stack

Preferred Shares: Not all Equal

Each priced round creates a new class of preferred stock with its own rights. They stack in reverse order at exit — the last investor in gets paid first.

• Paid 3rd at exit

• Weakest Rights Seed

Preferred

Liq. Preference

Anti-Dilution

Board Seat

Protective Provisions

Dividends

Pro-Rata Rights

Info Rights

1x Non-Participating

BBWA Standard

Rarely — Observer only

Narrow (3–5 items)

Often none

Major investors only

Basic annual financials

3rd in Waterfall

• Paid 2nd at exit

• Standard Rights Series A

Preferred

Liq. Preference

Anti-Dilution

Board Seat

Protective Provisions

Dividends

Pro-Rata Rights

Info Rights

1x — sometimes participating

BBWA - may push harder

1 Designated Seat

Standard NVCA (8–12)

6–8% cumulative, rarely paid

Standard — all investors

Full NVCA: monthly + audited

2nd in Waterfall

• Paid 1st at exit

• Strong Rights Series B

Preferred

Liq. Preference

Anti-Dilution

Board Seat

Protective Provisions

Dividends

Pro-Rata Rights

Info Rights

1-2x — Participating Preferred

May push for full ratchet

1 Additional Seat

Expanded + Layered veto

6–8% cumulative, rarely paid

Often super pro-rata

Full NVCA + tighter SLAs

1st in Waterfall

Governance

How you Lose Control

Board composition evolves at every priced round. Founders start with 100% of seats. By Series B, they're a minority — even if they still own the most equity.

Founding

2 seats · 100% founder

Pre-Seed

2 seats · SAFEs = no board seats

Seed

3 seats · Observer added, no vote

Series A

5 seats · Founders: 40%

Series A

7 seats · Founders: 28%

Founder Seat

Investor Seat

Independent Director

⚠ The Series A Inflection Point

Series A is where control structurally shifts. The standard 5-seat board (2 founders / 1 investor / 2 independents) means founders need the two independent directors on their side to pass any vote. Choose independent directors carefully — they're not neutral parties, they're swing votes on every significant company decision.

exit economics

The Liquidation Waterfall

At exit, proceeds don't flow to all shareholders equally. Preferred shareholders collect their full preference first — in reverse order of investment. Common shareholders (founders, employees) receive what's left.

PRIORITY

CLASS

GETS PAID

CONDITION

First

Series B Preferred

1–2x invested capital + participating upside

Before anyone else receives proceeds

EXAMPLE: Three Exit Scenarios

Assume: $2M Seed · $10M Series A · $25M Series B. Total preference stack = $37M. Founders + employees own 28% of common.

Below the stack$20M Exit

Series B

Series A

Seed

Common

$20M

0

0

0

Series B doesn't even recover full preference. All

other classes receive nothing.

Second

Series A Preferred

1x invested capital

After Series B is fully paid

Third

Seed Preferred

1x invested capital

After Series A is fully paid

Third

Common Shares

Everything remaining

Only after all preferred preferences satisfied

At the stack$40M Exit

Series B

Series A

Seed

Common

$25M

$10M

$2M

~$840K

Preferred fully paid. Founders share the $3M

remainder. A $40M exit barely moves the needle.

Above the stack$150M Exit

Series B

Series A

Seed

Common

$20M

$10M

$2M

~$32M

All preferences satisfied with room to spare.

Founders receive 28% of $113M remainder.

Hidden dilution

The option Pool Shuffle

Investors will ask you to create or expand an option pool before closing a priced round. Where that pool comes from is one of the most important — and least understood — points in term sheet negotiations.

Pre-Money Pool (What Investors Want)

The option pool is carved out of the pre-money valuation. It comes entirely out of the founders' shares. New investors' ownership percentage is calculated after the pool is set aside — so they never pay for it. You take 100% of the dilution.

Post-Money Pool (What Investors Want)

The option pool is created from the new shares issued in the round. Dilution is shared proportionally across all shareholders — founders and investors alike. This is harder to get but worth fighting for, especially on larger pool sizes.

Practical example: Investors ask for a 15% option pool at a $10M pre-money valuation. If it's carved pre-money, founders effectively accepted a $8.5M valuation for their shares — not $10M. On a $1M investment, that's a meaningful difference in actual dilution.

ready to Get This Right

From Day One?

Nerd Lawyer works with founders to build investor-ready legal infrastructure — from your first SAFE to your Series B. Clean caps, clean docs, no surprises at diligence.